Today I’m sharing details about a (new) popular financial scam.

To help you stay safe, I’m also sharing 3 ways to stay safe and protect yourself.

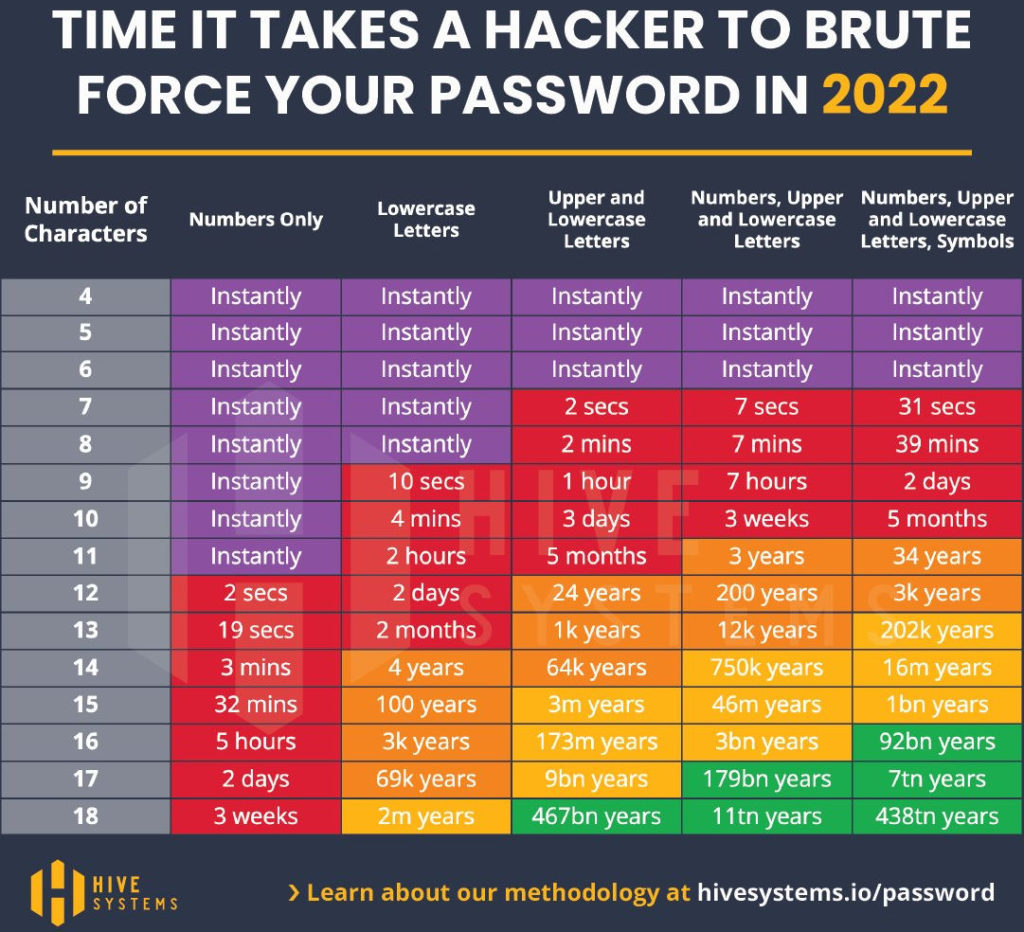

(Hint: your “complex” password may not be as secure as you think. 😲)

If you want to learn about this sophisticated financial scam + tips for protecting your family, this episode is for you.

When You’re Ready, Here Are 3 Ways I Can Help You:

- Schedule a Free Retirement Strategy Session. Get your questions answered + learn how we can help you improve retirement success and lower taxes.

- Listen to the Stay Wealthy Retirement Show. An Apple Top 50 investing podcast.

- Join My Retirement Newsletter. Weekly retirement and investing tips (delivered to our inbox!)

How to Listen to Today’s Episode

🎤 Click to Listen via Your Favorite Podcast App

Episode Links & Resources:

- Credit Freezes

- Free Credit Monitoring

- Password Managers

- Avast

- Hive Cybersecurity

- Password Guru Regrets Past Advice

- The Grandparent Scam