Inflation accelerated to 8.6% in May. 😬

Why is inflation getting worse? And how should retirement investors respond?

In this episode, I’m answering those questions + sharing key takeaways from the May inflation (CPI) report.

I’m also discussing:

- What “shadow inflation” is (and why you should ignore it)

- Why inflation is high

- What retirement investors can do in response

Age 50+? Need retirement + tax planning help? Get a Free Retirement Assessment👇

How to Listen to Today’s Episode

🎤 Click to Listen via Your Favorite Podcast App

Episode Resources:

- Stay Wealthy Inflation Series:

- Inflation Part 1 (2/9/22)

- Inflation Part 2 (2/22/22)

- Why I Was Wrong About Inflation (3/15/22)

- Shadow Inflation:

- Debunking Shadow Inflation [Full Stack Econ]

- Shadowstats Response to Errors [Econbrowser]

- Current CPI Report [U.S. Bureau of Labor Statistics]

- Federal Reserve Bank of San Francisco on Pandemic Relief and Inflation [BBC]

- How Not to Panic [Of Dollars and Data]

- Rising Interest Rates Don’t Mean Bonds Lose Money [Stay Wealthy]

- Why Are TIPS Losing Money [Stay Wealthy]

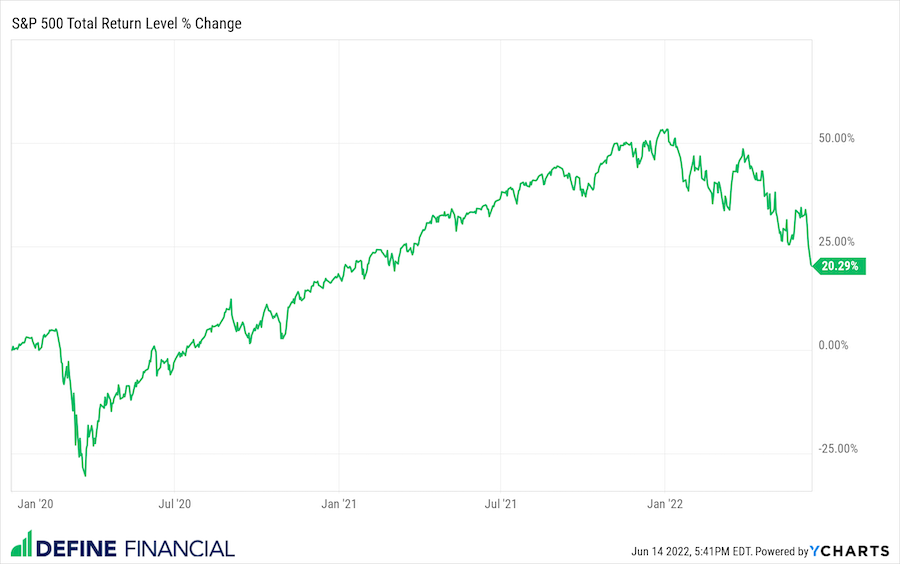

S&P 500 Total Return (1/1/20 – 6/13/22)